Blue Cross Blue Shield Advantage Nc Coverage 10000

Medicare Advantage enrollment has grown rapidly over the past decade, and Medicare Advantage plans have taken on a larger role in the Medicare program. This data analysis provides current information and trends about Medicare Advantage enrollment, premiums, and out-of-pocket limits. It also includes analyses of Medicare Advantage plans' extra benefits and prior authorization requirements. The analysis also highlights changes pertaining to Medicare Advantage coverage that have occurred in 2020 in response to the COVID-19 crisis.

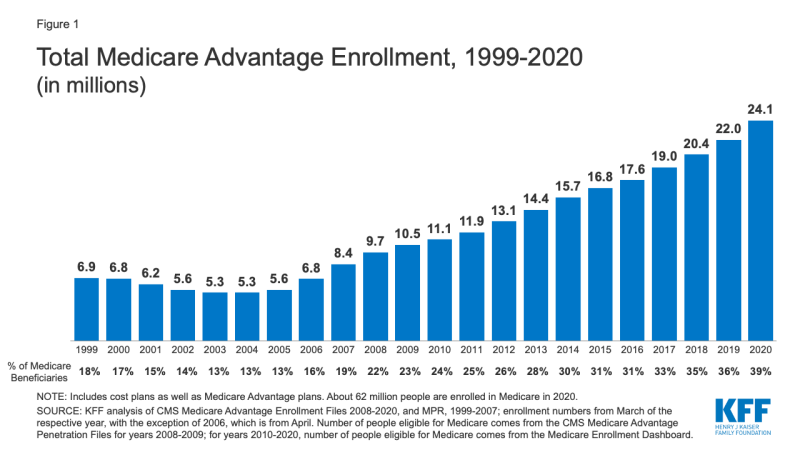

1. Enrollment in Medicare Advantage has doubled over the past decade

Figure 1: Total Medicare Advantage Enrollment, 1999-2020

In 2020, nearly four in ten (39%) of all Medicare beneficiaries – 24.1 million people out of 62.0 million Medicare beneficiaries overall – are enrolled in Medicare Advantage plans; this rate has steadily increased over time since the early 2000s. Between 2019 and 2020, total Medicare Advantage enrollment grew by about 2.1 million beneficiaries, or 9 percent – nearly the same growth rate as the prior year. The Congressional Budget Office (CBO) projects that the share of all Medicare beneficiaries enrolled in Medicare Advantage plans will rise to about 51 percent by 2030.

This analysis has been updated to reflect changes in methodology in how KFF calculates the total number of Medicare beneficiaries. These changes affected the share of Medicare beneficiaries enrolled in Medicare Advantage, as well as Medicare Advantage penetration by state and county. Please see methods section for more information.

Nearly one in five Medicare Advantage enrollees (19%) are in group plans offered by employers and unions for their retirees in 2020, roughly the same share since 2014. Under these arrangements, employers or unions contract with an insurer and Medicare pays the insurer a fixed amount per enrollee to provide benefits covered by Medicare. The employer or union (and sometimes the retiree) may also pay a premium for additional benefits or lower cost-sharing. Group enrollees comprise a disproportionately large share of Medicare Advantage enrollees in nine states: Alaska (100%), Michigan (49%), West Virginia (44%), New Jersey (40%), Wyoming (36%), Illinois (35%), Maryland (35%), Kentucky (34%), and Delaware (31%).

2. The share of Medicare beneficiaries in Medicare Advantage plans, by State, ranges from 1% to over 40%

The share of Medicare beneficiaries in Medicare Advantage plans (including Medicare cost plans), varies across the country. More than 40 percent of Medicare beneficiaries are enrolled in Medicare Advantage plans in nineteen states (FL, MN, HI, OR, WI, MI, AL, CT, PA, CA, CO, NY, OH, AZ, GA, TN, RI, TX, LA) and Puerto Rico. Medicare Advantage enrollment is relatively low (20 percent or lower) in nine states, including two mostly rural states where it is virtually non-existent (AK and WY).

Historically, the majority of Medicare private health plan enrollment in Minnesota has been in cost plans, rather than risk-based Medicare Advantage plans, but as of 2019, most cost plans in Minnesota are no longer offered and have been replaced with risk-based HMOs and PPOs.

Changes for 2020 due to COVID-19: The COVID-19 stimulus package, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, includes $100 billion in new funds for hospitals and other health care entities. The Centers for Medicare and Medicaid Services (CMS) has recently made $30 billion of these funds available to health care providers based on their share of total Medicare fee-for-service (FFS) reimbursements in 2019, resulting in higher payments to hospitals in some states than in others. Hospitals in states with higher shares of Medicare Advantage enrollees may have lower FFS reimbursement overall. As a result, some hospitals and other health care entities may be reimbursed less that they would if the allocation of funds took into account payments received on behalf of Medicare Advantage enrollees.

3. The share of Medicare beneficiaries in Medicare Advantage plans varies across counties from less than 1% to more than 70%

Within states, Medicare Advantage penetration varies widely across counties. For example, in Florida, 71 percent of all beneficiaries living in Miami-Dade County are enrolled in Medicare Advantage plans compared to only 14 percent of beneficiaries living in Monroe County (Key West).

In 117 counties, accounting for 5 percent of the Medicare population, more than 60% of all Medicare beneficiaries are enrolled in Medicare Advantage plans or cost plans. Many of these counties are centered around large, urban areas, such as Monroe County, NY (69%), which includes Rochester, and Allegheny County, PA (63%), which includes Pittsburgh.

In contrast, in 508 counties, accounting for 3 percent of Medicare beneficiaries, no more than 10 percent of beneficiaries are enrolled in Medicare private plans; many of these low penetration counties are in rural parts of the country. Some urban areas, such as Baltimore City (20%) and Cook County, IL (Chicago, 28%) have low Medicare Advantage enrollment, compared to the national average (39%).

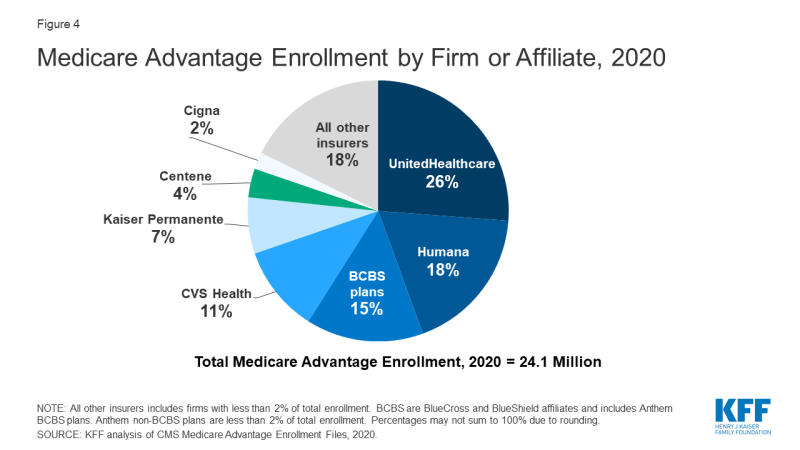

4. Most Medicare Advantage enrollees are in plans operated by UnitedHealthcare, Humana, or BlueCross BlueShield (BCBS) affiliates in 2020

Figure 4: Medicare Advantage Enrollment by Firm or Affiliate, 2020

Medicare Advantage enrollment is highly concentrated among a small number of firms. UnitedHealthcare and Humana together account for 44 percent of all Medicare Advantage enrollees nationwide, and the BCBS affiliates (including Anthem BCBS plans) account for another 15 percent of enrollment in 2020. Another four firms (CVS Health, Kaiser Permanente, Centene, and Cigna) account for another 23 percent of enrollment in 2020. For the fourth year in a row, enrollment in UnitedHealthcare's plans grew more than any other firm, increasing by more than 500,000 beneficiaries between March 2019 and March 2020. This is also the first year that Humana's increase in plan year enrollment was close to UnitedHealthcare's, with an increase of about 494,000 beneficiaries between March 2019 and March 2020. CVS Health purchased Aetna in 2018 and had the third largest growth in Medicare Advantage enrollment in 2020, increasing by about 396,000 beneficiaries between March 2019 and March 2020.

Changes for 2020 due to COVID-19: Medicare Advantage plans have flexibility to waive certain requirements with regard to coverage and cost sharing in cases of disaster or emergency, such as the COVID-19 outbreak. In response to the COVID-19 emergency, most Medicare Advantage insurers have announced that they are voluntarily waiving cost-sharing requirements for COVID-19 treatment.

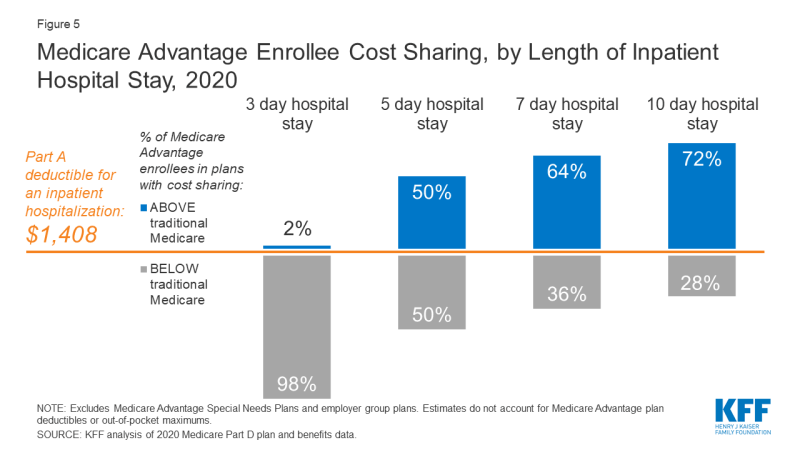

5. Half of all Medicare Advantage enrollees would incur higher costs than beneficiaries in traditional Medicare for a 5-day hospital stay

Figure 5: Medicare Advantage Enrollee Cost Sharing, by Length of Inpatient Hospital Stay, 2020

When Medicare Advantage enrollees require an inpatient hospital stay, many Medicare Advantage plans charge a daily copayment, beginning on day 1. Cost sharing requirements for Medicare Advantage enrollees also typically vary by length of stay. In contrast, under traditional Medicare, when beneficiaries require an inpatient hospital stay, there is a deductible of $1,408 in 2020 (for one spell of illness) with no copayments until day 60 of an inpatient stay.

In 2020, virtually all Medicare Advantage enrollees would pay less than the Part A hospital deductible for an inpatient stay of 3 days. But for stays of 5 days, among the half of Medicare Advantage enrollees required to pay more than the beneficiaries in traditional Medicare, those enrollees would pay $1,644 on average. Nearly two-thirds (64%) of Medicare Advantage enrollees are in a plan that requires higher cost sharing than the Part A hospital deductible in traditional Medicare for a 7-day inpatient stay, and more than 7 in 10 (72%) are in a plan that requires higher cost sharing for a 10-day inpatient stay.

Changes for 2020 due to COVID-19: Because the majority of Medicare Advantage firms have waived cost sharing for COVID-19 treatment, Medicare Advantage enrollees would not have to pay cost sharing if they require hospitalization due to COVID-19, though they would if they are hospitalized for other reasons. However, beneficiaries in traditional Medicare without supplemental coverage, would be responsible for any out-of-pocket costs relating to COVID-19 treatment if they are admitted to the hospital.

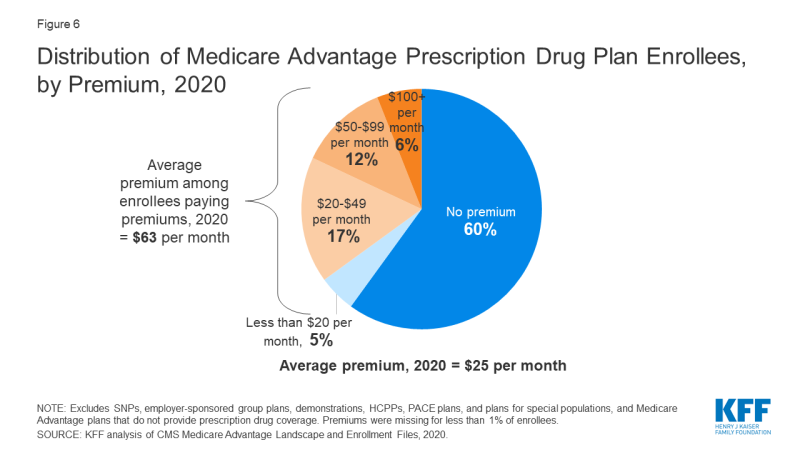

6. Nearly two-thirds of Medicare Advantage enrollees pay no supplemental premium (other than the Part B premium) in 2020

Figure 6: Distribution of Medicare Advantage Prescription Drug Plan Enrollees, by Premium, 2020

In 2020, 90% of Medicare Advantage plans offer prescription drug coverage (MA-PDs), and most Medicare Advantage enrollees (89%) are in plans that include this prescription drug coverage. Nearly two-thirds of these beneficiaries (60%) pay no premium for their plan, other than the Medicare Part B premium ($144.60 in 2020). However, 18 percent of beneficiaries in MA-PDs (2.8 million enrollees) pay at least $50 per month, including 6 percent who pay $100 or more per month, in addition to the monthly Part B premium. The MA-PD premium includes both the cost of Medicare-covered Part A and Part B benefits and Part D prescription drug coverage. Among MA-PD enrollees who pay a premium for their plan, the average premium is $63 per month. Altogether, including those who do not pay a premium, the average MA-PD enrollee pays $25 per month in 2020.

Changes for 2020 due to COVID-19: During the duration of the COVID-19 public health emergency, Medicare Part D plans, including MA-PDs and stand-alone drug plans, are required to provide up to a 90-day (3 month) supply of covered Part D drugs to enrollees who request it to make it easier for beneficiaries to shelter in place, without taking unnecessary trips to the pharmacy to fill a prescription.

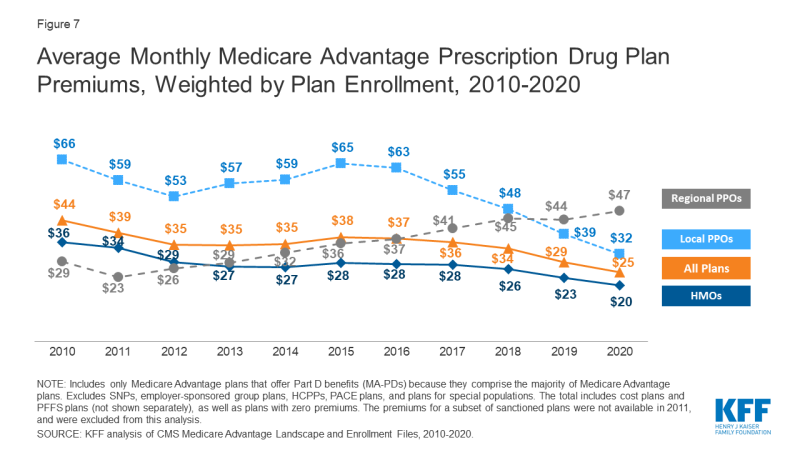

7. Premiums paid by Medicare Advantage enrollees have slowly declined since 2015

Figure 7: Average Monthly Medicare Advantage Prescription Drug Plan Premiums, Weighted by Plan Enrollment, 2010-2020

Nationwide, average Medicare Advantage Prescription Drug (MA-PD) premiums declined by $4 per month between 2019 and 2020, much of which was due to the relatively sharp decline in premiums for local PPOs this past year. Average premiums for HMOs also declined $3 per month, while premiums for regional PPOs increased $3 per month between 2019 and 2020.

Average MA-PD premiums vary by plan type, ranging from $20 per month for HMOs to $32 per month for local PPOs and $47 per month for regional PPOs. Nearly two-thirds (61%) of Medicare Advantage enrollees are in HMOs, 33% are in local PPOs, and 5% are in regional PPOs in 2020.

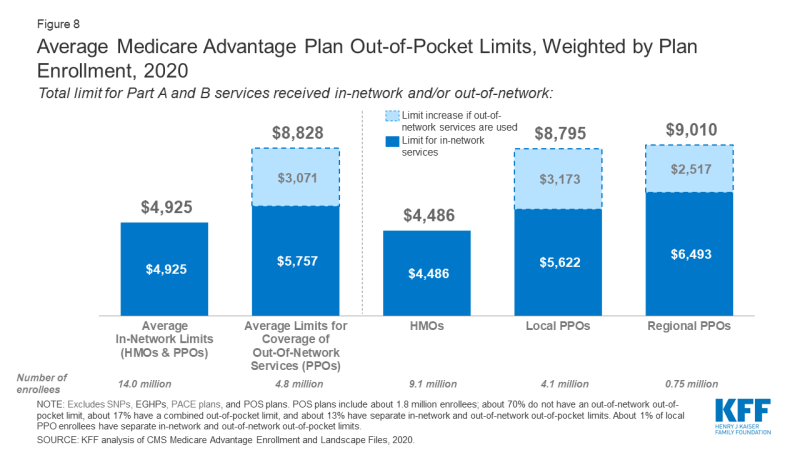

8. For Medicare Advantage enrollees, the average out-of-pocket limit is $4,925 for in-network services and $8,828 for both in-network and out-of-network services (PPOs)

Figure 8: Average Medicare Advantage Plan Out-of-Pocket Limits, Weighted by Plan Enrollment, 2020

In 2020, Medicare Advantage enrollees' average out-of-pocket limit for in-network services is $4,925 (HMOs and PPOs) and $8,828 for out-of-network services (PPOs). For HMO enrollees, the average out-of-pocket (in network) limit is $4,486; these plans do not cover services received from out-of-network providers. For local and regional PPO enrollees, the average out-of-pocket limit for both in-network and out-of-network services are $8,795, and $9,010, respectively. These out-of-pocket limits apply to Part A and B services only, and do not apply to Part D spending.

HMOs generally only cover services provided by in-network providers, whereas PPOs also cover services delivered by out-of-network providers but charge enrollees higher cost-sharing for this care. The size of Medicare Advantage provider networks for physicians and hospitals vary greatly both across counties and across plans in the same county.

Average overall out-of-pocket limits for in-network services has trended down from 2017 – with the largest decrease for HMOs (down from $4,976 in 2017 to $4,486 in 2020). Out-of-network limits for PPOs (which provide coverage for out-of-network services) have also decreased since 2017 (down from $9,073 in 2017 to $8,828 in 2020).

Since 2011, federal regulation has required Medicare Advantage plans to provide an out-of-pocket limit for services covered under Parts A and B not to exceed $6,700 (in-network) or $10,000 (in-network and out-of-network combined). Beginning next year, in 2021, these limits will increase to $7,550 (in-network) and $11,300 (in-network and out-of-network) due to changes in eligibility for beneficiaries with End Stage Renal Disease (ESRD) who will, for the first time, be able to enroll in Medicare Advantage plans. Beneficiaries with diagnoses of ESRD typically incur higher costs than the average beneficiary, and CMS is making these changes to out-of-pocket maximums to better reflect beneficiary spending.

Changes for 2020 due to COVID-19: In light of the declaration of a public health emergency in response to the coronavirus pandemic, certain special requirements with regard to out-of-network services are in place. During the period of the declared emergency, Medicare Advantage plans are required to cover services at out-of-network facilities that participate in Medicare, and charge enrollees who are affected by the emergency and who receive care at out-of-network facilities no more than they would face if they had received care at an in-network facility.

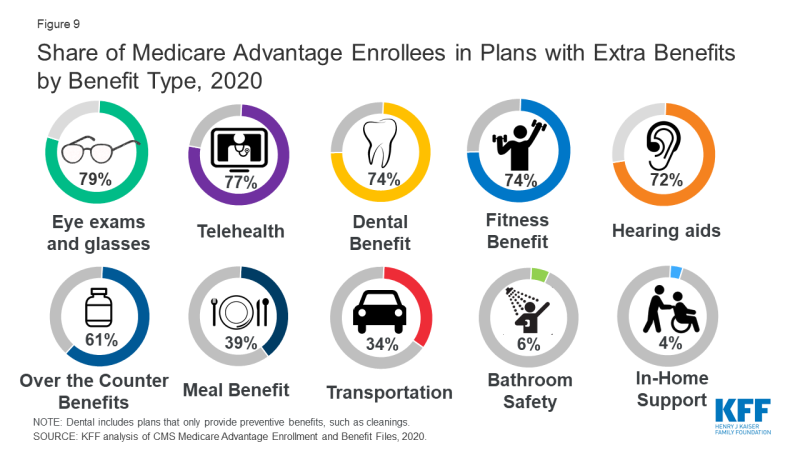

9. Most Medicare Advantage enrollees have access to some benefits not covered by traditional Medicare in 2020

Figure 9: Share of Medicare Advantage Enrollees in Plans with Extra Benefits by Benefit Type, 2020

Medicare Advantage plans may provide extra ("supplemental") benefits that are not offered in traditional Medicare, and can use rebate dollars to help cover the cost of extra benefits. Plans can also charge additional premiums for such benefits. Beginning in 2019, Medicare Advantage plans have been able to offer additional supplemental benefits that were not offered in previous years. These supplemental benefits must still be considered "primarily health related" but CMS expanded this definition, so more items and services are available as supplemental benefits.

Most enrollees are in plans that provide access to eye exams or glasses (79%), telehealth services (77%), dental care (74%), a fitness benefit (74%), and hearing aids (72%). Since 2010, the share of enrollees in plans that provide some dental care, fitness benefits, or hearing aids has increased (from 48%, 52%, and 37% of enrollees, respectively) while the share with a vision benefit has been relatively steady (77% in 2010).

Changes for 2020 due to COVID-19: CMS is allowing the expansion of mid-year benefit enhancements, such as additional or expanded benefits or more generous cost sharing, as long as they are in connection with the COVID-19 public health emergency. For example, Medicare Advantage plans may add transportation benefits or meal delivery services to promote social distancing during the COVID-19 outbreak. Many are also expanding telehealth services and are waiving or reducing cost sharing for telehealth services. Changes that have occurred since the start of the plan year, including changes to telehealth adopted by plans in response to the pandemic, are not reflected in the data used for this analysis.

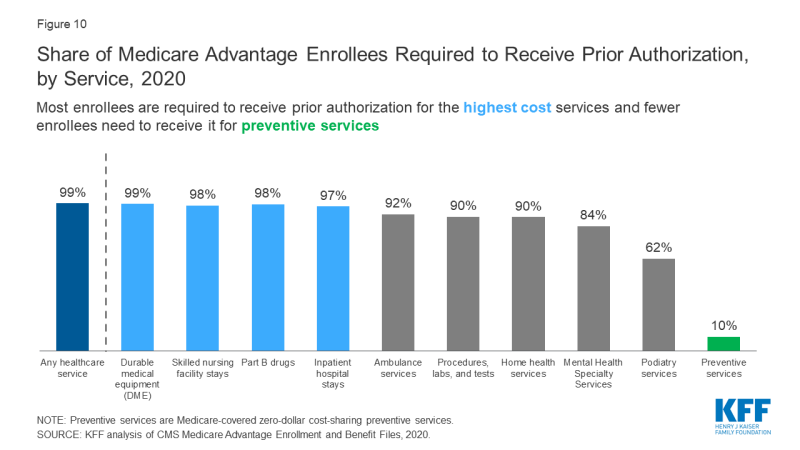

10. Nearly all Medicare Advantage enrollees are in plans that require prior authorization for some services

Figure 10: Share of Medicare Advantage Enrollees Required to Receive Prior Authorization, by Service, 2020

Medicare Advantage plans can require enrollees to receive prior authorization before a service will be covered, and nearly all Medicare Advantage enrollees (99%) are in plans that require prior authorization for some services in 2020. Prior authorization is most often required for relatively expensive services, such as inpatient hospital stays, skilled nursing facility stays, and Part B drugs, and is infrequently required for preventive services. The number of enrollees in plans that require prior authorization for one or more services increased from 2019 to 2020, from 79% in 2019 to 99% in 2020. In contrast to Medicare Advantage plans, traditional Medicare does not generally require prior authorization for services, and does not require step therapy for Part B drugs.

Changes for 2020 due to COVID-19: In response to the COVID-19 public health emergency, several Medicare Advantage plans have waived prior authorization requirements for individuals needing treatment for COVID-19.

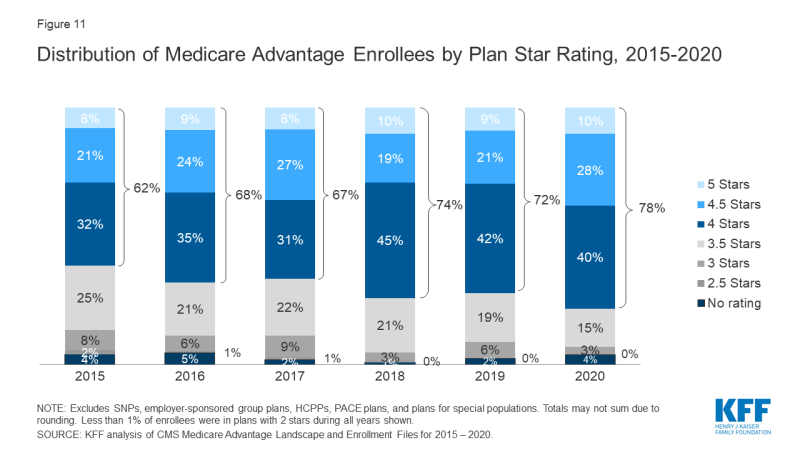

11. The majority (78%) of Medicare Advantage enrollees are in plans that receive high quality ratings (4 or more stars) and related bonus payments

Figure 11: Share of Medicare Advantage Enrollees Required to Receive Prior Authorization, by Service, 2020

In 2020, more than three-quarters (78%) of Medicare Advantage enrollees are in plans with quality ratings of 4 or more stars, an increase from 2019 (72%). An additional 4 percent of enrollees are in plans that were not rated because they were part of contracts that had too few enrollees or were too new to receive ratings. Plans with 4 or more stars and plans without ratings are eligible to receive bonus payments for each enrollee the following plan year. The share of enrollees in plans with 3 stars (average ratings) declined by half from 6 percent in 2019 to 3 percent in 2020.

For many years, CMS has posted quality ratings of Medicare Advantage plans to provide beneficiaries with additional information about plans offered in their area. All plans are rated on a 1 to 5-star scale, with 1 star representing poor performance, 3 stars representing average performance, and 5 stars representing excellent performance. CMS assigns quality ratings at the contract level, rather than for each individual plan, meaning that each plan covered under the same contract receives the same quality rating; most contracts cover multiple plans.

Changes for 2020 due to COVID-19: Due to the COVID-19 emergency, CMS has issued an Interim Final Rule that will modify the calculation of the 2021 and 2022 Medicare Advantage Star Ratings to address the expected disruption to data collection and measure scores, and avoid creating incentives that, according to CMS, might lead plans to place cost considerations above patient safety.

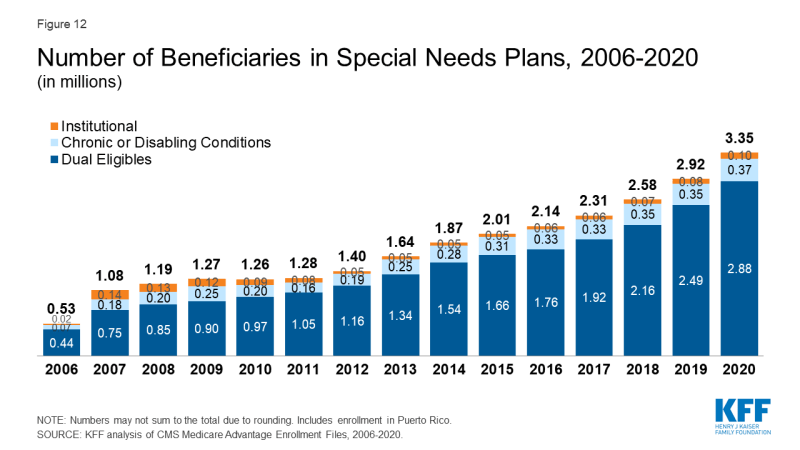

12. More than 3 million Medicare beneficiaries are enrolled in Special Needs Plans in 2020

Figure 12: Number of Beneficiaries in Special Needs Plans, 2006-2020

More than three million Medicare beneficiaries are enrolled in Special Needs Plans (SNPs). SNPs restrict enrollment to specific types of beneficiaries with significant or relatively specialized care needs. The majority of SNP enrollees (86%) are in plans for beneficiaries dually eligible for Medicare and Medicaid (D-SNPs), Another 11 percent of enrollees are in plans for people with severe chronic or disabling conditions (C-SNPs) and 3 percent are in plans for beneficiaries requiring a nursing home or institutional level of care (I-SNPs).

Enrollment in SNPs increased from 2.9 million beneficiaries in 2019 to 3.3 million beneficiaries in 2020 (15% increase), accounting for about 14 percent of total Medicare Advantage enrollment in 2020, with some variation across states. In nine states, the District of Columbia, and Puerto Rico, enrollment in SNPs comprises at least one-fifth of Medicare Advantage enrollment (55% in DC, 48% in PR, 23% in SC, 23% in NY, 21% in AR, 21% in GA, 21% in MS, 20% in AZ, 20% in FL, 20% in LA, and 20% in TN). Most C-SNP enrollees (94%) are in plans for people with diabetes or cardiovascular disorders in 2020. Enrollment in I-SNPs has been increasing but is still fewer than 100,000 beneficiaries in 2020.

Changes for 2020 due to COVID-19: In response to the public health emergency, CMS will use discretion when enforcing certain oversight and monitoring activities relating to SNPs, including if Medicare Advantage plans do not fully comply with their approved SNP model of care (MOC) or if plans experience delays in recertifying SNP eligibility.

Meredith Freed and Tricia Neuman are with KFF.

Anthony Damico is an independent consultant.

| Data and Methods |

| This analysis uses data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Enrollment, Benefit and Landscape files for the respective year. KFF is now using the Medicare Enrollment Dashboard for enrollment data, from March of each year. In previous years, KFF has used the Medicare Advantage Penetration Files to calculate the number of Medicare beneficiaries eligible for Medicare. The Medicare Advantage Penetration Files includes people who were previously, but no longer covered by Medicare (e.g., people who obtained employer-sponsored health insurance coverage after initially enrolling in Medicare). It also includes people within 5 months of their 65th birthday, but not yet age 65. In addition, CMS has identified an issue where beneficiaries with multiple addresses were double counted in the Penetration File. KFF has refined its approach this year and is using the Medicare Enrollment Dashboard to calculate the number of Medicare beneficiaries because it only includes Medicare beneficiaries with either Part A or Part B coverage, which is a more accurate estimate of the Medicare population. The numbers published here supersede all prior estimates by KFF of the number of Medicare beneficiaries. Cost plans are grouped with Medicare Advantage plans, and this analysis uses the term Medicare Advantage to refer to both types of plans, even though cost plans are paid differently and subject to different rules. Enrollment counts in publications by firms operating in the Medicare Advantage market, such as company financial statements, might differ from KFF estimates due to inclusion or exclusion of certain plan types, such as SNPs or employer plans. |

obrienfromastlese.blogspot.com

Source: https://www.kff.org/medicare/issue-brief/a-dozen-facts-about-medicare-advantage-in-2020/

0 Response to "Blue Cross Blue Shield Advantage Nc Coverage 10000"

Postar um comentário